What Veterans in Delaware & Pennsylvania Should Know About Their VA Home Loan Benefit

For many Veterans across Delaware and Pennsylvania, buying a home can feel overwhelming in today’s market.

Between rising prices, interest rates, and the idea of needing a large down payment, many buyers assume homeownership is years away. But for eligible Veterans, the VA home loan benefit may make buying sooner more realistic than expected.

According to a recent survey from NewDay USA, nearly half of Veterans feel homeownership is currently out of reach. At the same time, many are unaware of the full advantages their VA benefit provides.

Whether you’re looking in Wilmington, Newark, Middletown, Dover, West Chester, or nearby Pennsylvania communities, understanding how a VA loan works could significantly change your homebuying strategy.

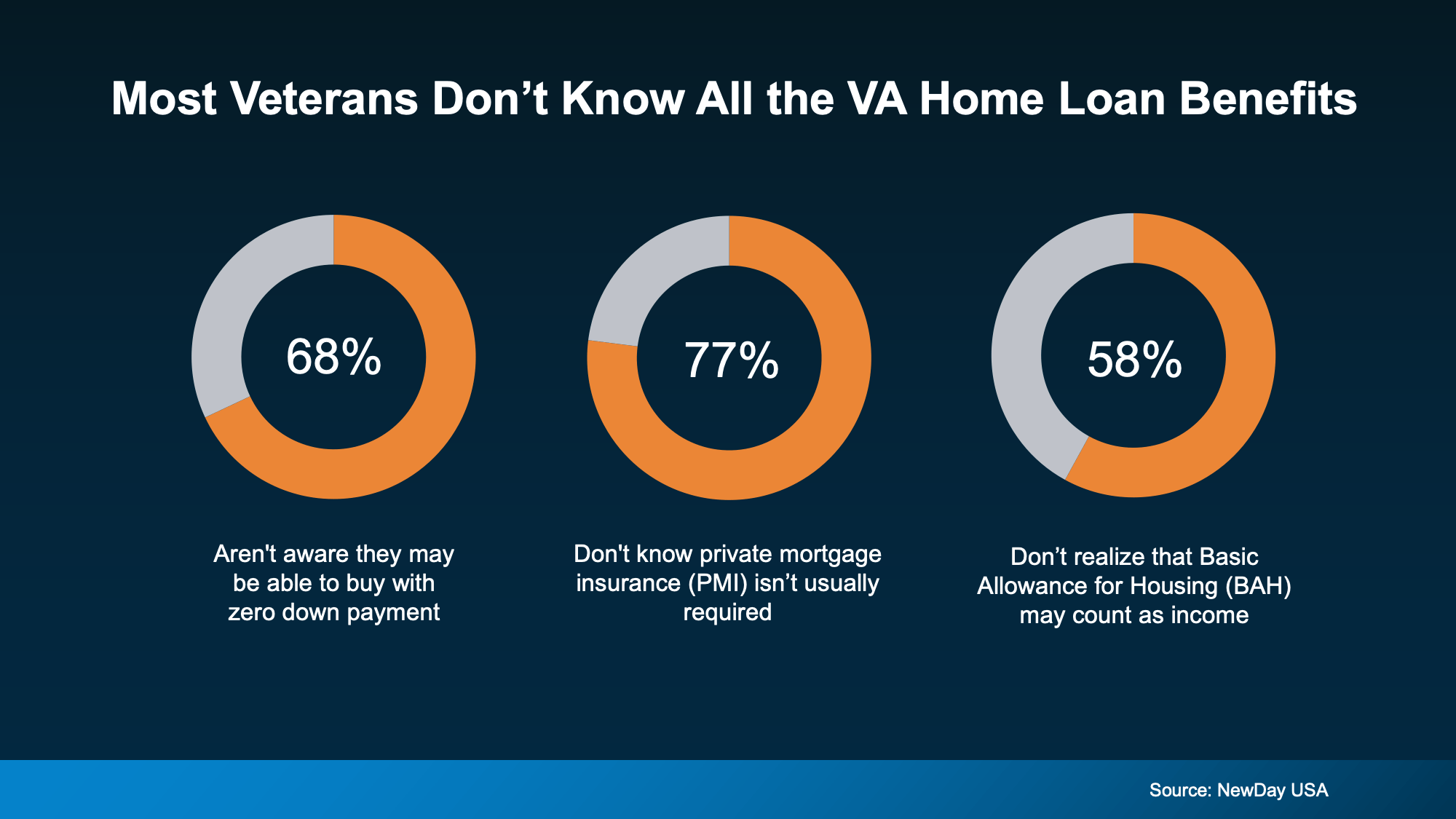

Veterans don’t know all the VA home loan benefits graphic

You May Not Need a Large Down Payment

One of the biggest misconceptions about buying a home is that you need a large amount saved upfront.

For eligible Veterans, VA loans may allow buyers to purchase a home with little to no down payment.

In growing markets throughout Delaware and Pennsylvania, where buyers are trying to balance affordability with rising home values, this can be a major advantage.

Instead of waiting years to save, some Veterans may already be closer to buying than they realize.

VA Loans Can Help Lower Upfront Costs

Closing costs can add up quickly during the homebuying process.

The VA loan program places limits on certain fees and costs buyers may be required to pay, helping many Veterans reduce upfront expenses compared to other loan types.

For buyers trying to navigate competitive Delaware and Pennsylvania markets, keeping more money in savings can create added flexibility and confidence during the process.

No PMI Can Mean Lower Monthly Payments

Many conventional loans require private mortgage insurance (PMI) when buyers put down less than 20%.

VA loans typically do not require PMI, even with low or zero down payment options.

That monthly savings can make a meaningful difference for homeowners, especially when budgeting for future expenses, renovations, or everyday living costs.

BAH & BAS May Increase Buying Power

For active duty military members and qualifying reservists, BAH and BAS allowances may count toward qualifying income.

Because these benefits are non-taxable, they can potentially help buyers qualify for a higher purchase price than they initially expected.

That added purchasing power may open up more opportunities across Delaware and Pennsylvania communities.

Bottom Line

The VA home loan benefit remains one of the most powerful tools available to Veterans and active duty military members.

If you’ve served, are currently serving, or know someone who has, understanding these benefits could make homeownership more achievable than expected.

Whether you’re buying your first home, relocating, or planning your next move in Delaware or Pennsylvania, connecting with a trusted lender and knowledgeable local real estate professional can help you better understand your options and create a strategy that works for your goals.