What Many Baltimore Veterans Don’t Know About Their VA Home Loan Benefit

For many Veterans in Baltimore and across Maryland, homeownership can feel harder than ever. Between rising home prices, interest rates, and the pressure to save for upfront costs, it’s easy to assume buying a home is out of reach.

But for many Veterans, that may not actually be the case.

According to a recent survey from NewDay USA, nearly half of Veterans (49%) feel homeownership is currently unattainable. The surprising part? Many may already qualify for benefits that could make buying a home much more achievable.

The VA home loan program has been around for more than 80 years, yet many buyers still misunderstand how it works and what it offers.

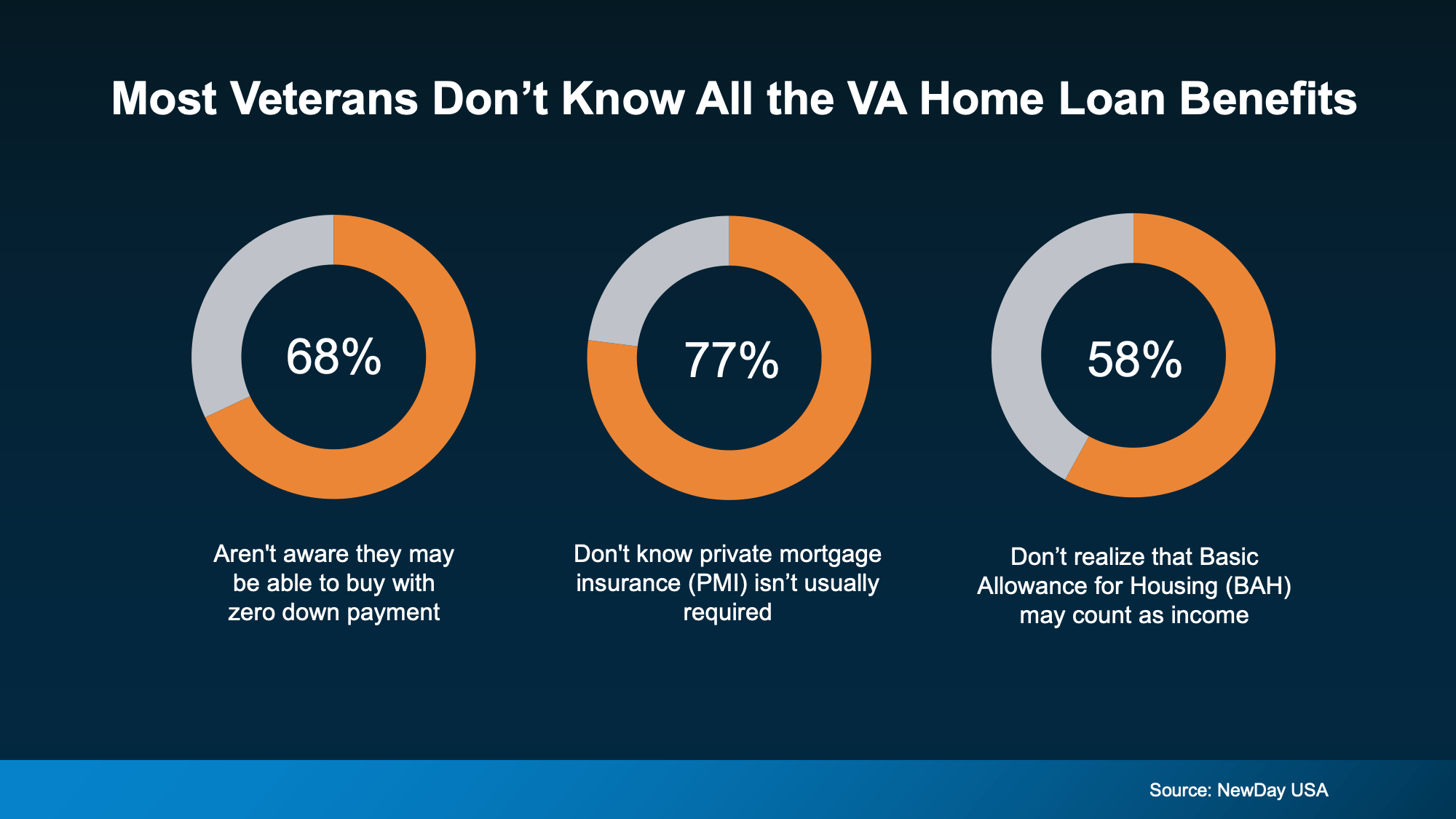

Here are some of the biggest misconceptions we hear from Veterans throughout Baltimore, South Baltimore, Federal Hill, Locust Point, Canton, and surrounding Maryland communities.

You May Not Need a Down Payment

One of the biggest advantages of a VA loan is the ability to purchase a home with little to no money down.

Many buyers assume they need to save tens of thousands of dollars before buying in neighborhoods like Riverside, Canton, or Towson. While saving is always helpful, VA loans can eliminate one of the biggest barriers to entry for eligible buyers.

That means Veterans may be able to become homeowners sooner than they expected.

VA Loans Can Help Reduce Closing Costs

Closing costs are another area that catches many buyers off guard.

With VA loans, there are limits on certain fees and closing costs buyers may have to pay. In a competitive Maryland real estate market, this can help Veterans keep more cash available for moving expenses, repairs, furnishings, or future savings.

Combined with low down payment options, this benefit can make homeownership far more accessible.

You May Not Have To Pay PMI

Many conventional loans require private mortgage insurance (PMI) when buyers put down less than 20%.

VA loans typically do not require PMI, even with low or no down payment.

That can save homeowners hundreds of dollars every month — money that can instead go toward building equity, home improvements, or everyday expenses.

Active Duty Buyers May Qualify for More Than They Think

For active duty service members and qualifying reservists, Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification.

Since BAH and BAS are non-taxable allowances, they can increase purchasing power and potentially help buyers qualify for more than they initially expected.

This can be especially important in competitive Baltimore-area markets where understanding your true buying power matters.

Bottom Line

VA home loans continue to be one of the most valuable benefits available to Veterans and active duty military members.

Whether you’re considering buying your first home in Baltimore, upgrading into a larger property, or simply exploring your options in Maryland, understanding your VA loan benefit could open doors you didn’t realize were possible.

If you’ve served or are currently serving, connecting with a trusted lender and local real estate professional can help you understand exactly what options are available and how to make the most of your benefits.